INSIGHT ARTICLE

Road to Net Zero Study: An executive summary

By Basil Choudhry, Commercial Director

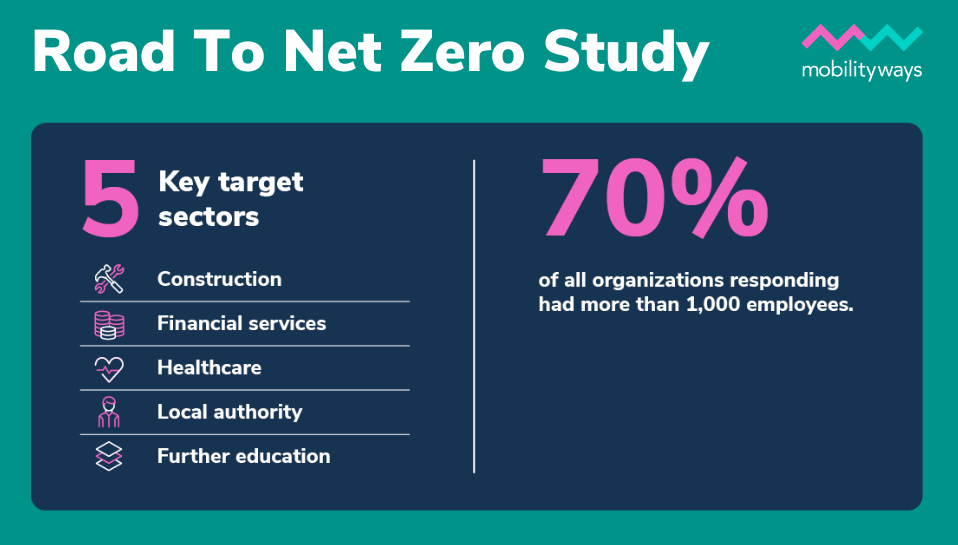

During the early part of 2023, Mobilityways decided to explore the progress of large organisations in addressing decarbonisation in their operations and supply chains. We wanted to run some highly robust business-to-business market research across five key sectors where Mobilityways already has a growing presence.

To do this, we decided to work with the highly respected research agency Opinium. Respondents needed to employ a minimum of 500 people. In fact, over two thirds of respondents to the market research Opinium carried out in the Spring employed over 1,000 people.

We sought to approach a representative sample of at least 50 companies in each of the target sectors: local authorities, further education, the NHS/healthcare, financial services and construction/civil engineering. In the latter three sectors, we were able to reach 100 relevant senior sustainability or transport decision professionals within 100 different large organisations.

There are as many ways to reduce emissions as there are sources of Scope 1, 2 and 3 emissions, as defined initially by the Greenhouse Gas Protocol back in 2001. As the commuter emission solutions specialists, Mobilityways recognises that some drivers for change are more powerful than others, perhaps according to the sector you operate in or the preferred approach of senior management.

Why is this necessary?

It is becoming increasingly undeniable that rapid decarbonisation, combined with the development of greener energy alternatives, gives us the best chance of limiting global warming to 1.5°C above pre-industrial levels.

According to the Intergovernmental Panel on Climate Change (IPCC), if we can contain global warming to 1.5 °C above pre-industrial levels and develop related global greenhouse gas (GHG) emission pathways, approximately 420 million fewer people will be frequently exposed to extreme heatwaves, and about 65 million fewer people will be exposed to exceptional heatwaves.

There is now a 32 per cent chance that the average temperature over the next five years will exceed the 1.5°C threshold.

It is also becoming clear that decarbonisation is increasingly urgent. The odds of temporarily exceeding 1.5 °C have been rising since 2015. Between 2017 and 2021 there was a 10 per cent chance of exceeding this key threshold. However, fast forward to 2023 and there is now a 32 per cent chance that the average temperature over the next five years will exceed the 1.5°C threshold.

Some cultures prefer to encourage staff to find ways to reduce their employers’ overall carbon footprint. Others are more inclined to prescribe changes and impose penalties on staff that don’t do the right thing. Whatever the approach, it is becoming increasingly clear that continuing burning fossil fuels at the rate we have been is self-defeating.

What does the study capture?

This study explores at what stage large UK-based firms have reached in terms of Scope 1, 2 and 3 Greenhouse Gas (GHG) emissions reporting. We’ve also asked them which overarching ESG reporting frameworks they are using.

It asks key sustainability decision makers for their views on the differing reporting systems in use – exploring their concerns about the accuracy and comparability of current measurement systems. We also looked at the level of benchmarking already in place to help large firms compare their performance and emissions reduction record with peers within their sector.

We were also able to gather data about the level and extent of employee commute emissions reporting being done so far – exploring any plans to encourage staff to select greener alternatives including car sharing, cycling, and use of public transport where possible. So, let’s get into some of the more eye catching findings.

You might also enjoy:

2023 Commuter Census: An executive summary

Calculating the ROI of sustainable commuting

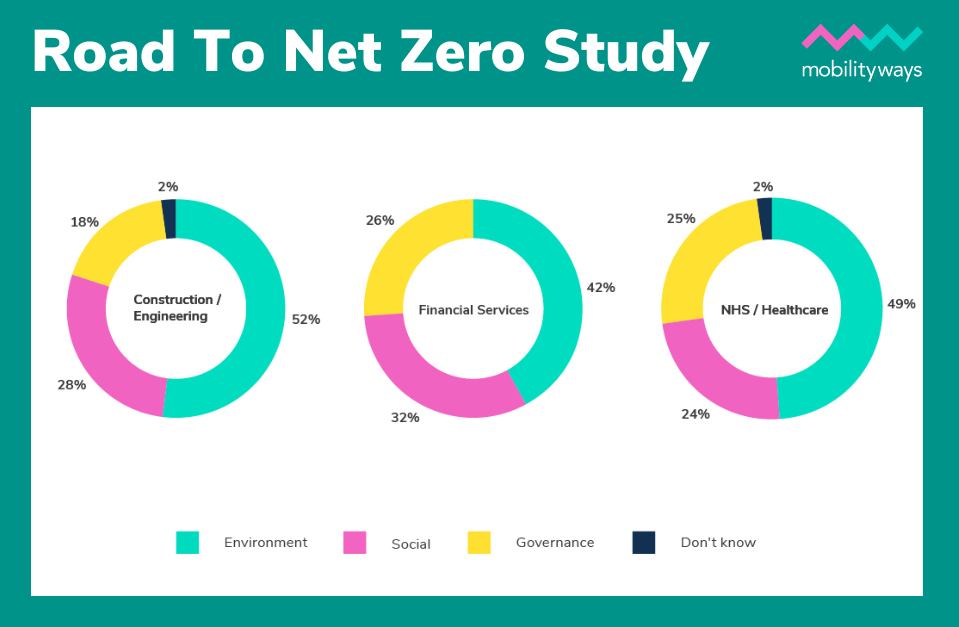

Fig 1. Which of the three core ESG factors do you think your organisation has made most progress with in terms of finding reliable ways to measure, monitor and report on progress against stated goals?

Just 1.5% on top of all Scope 1, 2 and 3 reporting

Just 1.5 per cent of the organisations with more than 1,000 staff that had begun environmental reporting using a recognised ESG reporting framework, felt they had ‘a strong handle on all our Scope 1, 2 and 3 reporting systems and processes’. Less, just one per cent of businesses with 501 to 1,000 employees, felt they were on top of all Scope 1, 2, and 3 emissions reporting systems and processes, the April 2023 study found.

Scope 3 reporting implementation is only about halfway complete

Just over half (55 per cent) of the largest UK enterprises who had begun Scope 3 reporting implementation had already ‘studied the impact of our products after use and used this data to redesign how we make our products’. Slightly less, 53 per cent, had ‘audited all their suppliers’ emissions data to verify accuracy using a single universal reporting framework’.

Just over 50 per cent had ‘worked out a way of measuring Greenhouse Gas (GHG) emissions from employee commutes to and from their place of work’. Under half (47 per cent) had completed analysis of ‘all our suppliers and asked them to provide us with relevant emissions data regularly’. Marginally less, 48 per cent, had fully implemented the Greenhouse Gas Protocol’s Corporate Value Chain (Scope 3) Accounting & Reporting Standard.

Just 1.5 per cent of the organisations with more than 1,000 staff that had begun environmental reporting using a recognised ESG reporting framework, felt they had ‘a strong handle on all our Scope 1, 2 and 3 reporting systems and processes’.

Average of 3.5 different ESG reporting frameworks in use

Mobilityways also explored which ESG reporting frameworks these large companies were using and found that on average they had used 3.5 different ESG reporting frameworks each. However, opinions on which framework was best varied according to the sector they were in. For example, the financial services firms judged the Sustainability Accounting Standards Board (SASB) ESG guidance framework ‘the most useful’ for them: a quarter (26 per cent) of financial services firms favoured SASB over others they’ve used. Other sectors favoured different reporting frameworks.

Lack of reporting standardisation proves big concern

The lack of standardisation for weighting and measuring emissions performance, especially with regards to Scope 3, was the most significant concern with the environmental performance reporting systems firms were using, as clear evidence emerged of a spaghetti soup of different ESG reporting frameworks, standards and sector certification systems being applied across many large organisations.

56 per cent of 1000+ employee firms cited this lack of standardisation for Scope 3 reporting as a top concern. While just over half (52 per cent) of these largest firms were having difficulties turning all the emissions data into actionable insights, admitting ‘we don’t really know the story behind the numbers’ yet.

Data accuracy still a concern, especially for supply chain data

Just under half (49 per cent) of large companies expressed concern about the accuracy of existing environmental performance scoring and ratings systems they were using. Meanwhile, 47 per cent recorded ‘gaps in provision of our (own) organisation’s and (their) suppliers’ environmental performance records’.

Scope 1 & 2 benchmarking possible for two thirds of large firms

Nearly two thirds (65 per cent) of 1,000+ employee firms were able to compare their Scope 1 and 2 reports with a sector average for key factors making up direct emissions. The construction and civil engineering sector respondents fared better still, with 72 per cent of this sector reporting they could run their numbers against construction sector averages by emission category to help assess their performance.

When drilling into large organisations that have already implemented Scope 1 and 2 reporting, it became clear that more than a third of these firms were not yet able to run peer group or sector benchmarking for key emissions categories. For example, 36 per cent of the largest firms already doing Scope 1 and 2 reporting admitted they could not benchmark their results associated with GHG Emissions Impact.

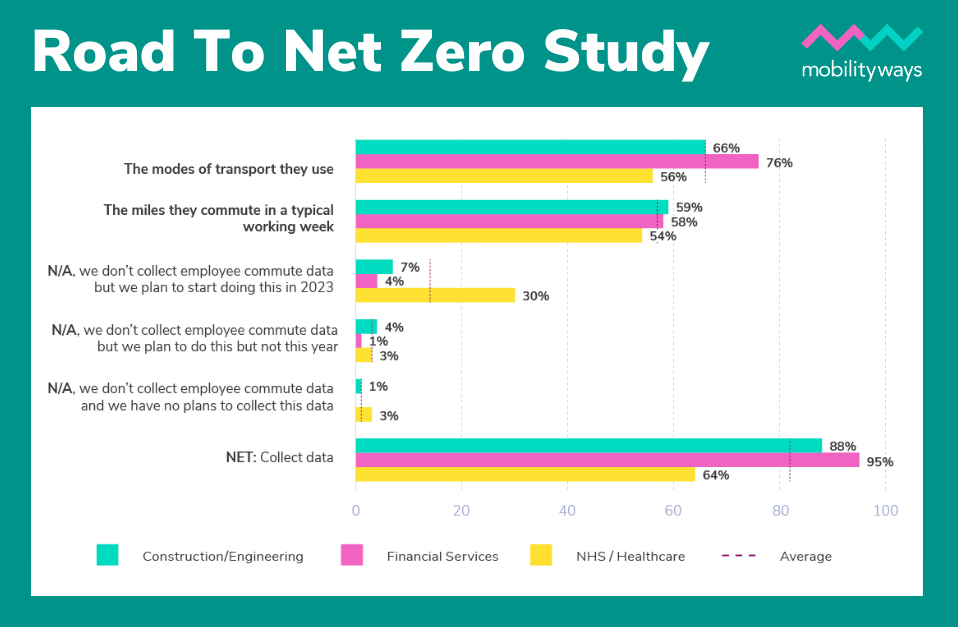

Fig 2. What employee commuting data do you currently collect?

Scope 3 benchmarking proving harder than Scope 1 & 2

In terms of Scope 3 benchmarking, it was clear that the 1,000+ employee companies were finding it much more difficult to check their performance against sector averages across all key factors than smaller firms with 501 to 1,000 employees.

For example, only 61 per cent of those largest companies were capable of comparing their employee commute emission results with sector averages. Meanwhile, amongst firms employing between 501 and 1,000 staff that had implemented Scope 3 reporting already, 79 per cent were already capable of benchmarking their emissions reduction performance for employee commuting.

There is still some reticence around addressing Scope 3 indirect emissions. Yet those firms that have begun to address this work head on are finding there are massive emissions reductions to be realised. Some authoritative studies have found Scope 3 emissions, in some large global organisations, can account for as much as 85 per cent of their total emissions.

Key takeaways

Mobilityways’ Road to Net Zero Study’s findings show that less than two thirds of the largest firms have begun implementing Scope 3 reporting, and those that have begun doing so are only about halfway through working out how to collect and evaluate all the data they need.

Settling on the right ESG reporting systems for both them and their value chains is also proving tricky, and many firms are using different reporting systems in parallel to suit the needs of different stakeholders they need to report to. They’re midway through a complex journey to gather the right data and report it in a universally comprehensive manner. No wonder some corporations’ annual ESG reports are already running to more than 100 pages!

Some authoritative studies have found Scope 3 emissions, in some large global organisations, can account for as much as 85 per cent of their total emissions.

We also found that sustainability chiefs calculated that, on average, they expected that 38 per cent of total emissions would be Scope 3 emissions. That looks like a significant underestimate based on a number of expert industry studies.

However, the key point remains that companies can reduce their Scope 3 emissions very rapidly by addressing Upstream Scope 3 categories such as employee commute emissions which are more in their control than many of their suppliers’ emissions reports.

The key is to start measuring what you can fast, thereby working out the scale of the emissions reduction opportunity for you, and then kick off initiatives to chip away at reductions in the categories you can affect. We can even help firms benchmark their employee commute performance against similar sized businesses in a given region of the UK for example.

We are conscious that in this summary of results we have not been able to spare the space to summarise some of the sector-specific findings. However, be assured the core Management Report has extensive sector-specific findings, especially for the healthcare and construction sectors which have their own dedicated chapters.

Please do get in touch if you would like to hear more about how Mobilityways is helping large organisations to reduce the carbon emissions of their commuters, particularly now that more workers are returning to their offices more regularly, as pandemic-linked work-from-home regimes are adjusted in favour of hybrid working arrangements.

Start your Zero Carbon Commuting journey with a free consultation with one of our Commutologists

Get in touch now

Tell us a little more about your company, and we’ll call you back.